The Kolkata-based UCO Bank has come under the scanner of the Reserve Bank of India (RBI). The RBI, the apex bank of the country regulating all scheduled commercial banks, has hauled up UCO Bank in its Annual Financial Inspection Report (AFIR) for 2001-06. The report reveals that there has been large-scale understate ment of Non-Performing Assets (NPAs) by the bank during this period.The bank has routinely been making less provi sions for NPAs than required by RBI guidelines.For instance, a review of 48 and 44 stressed assets for 2004-05 and 2005 06, respectively, shows that the bank has understated NPAs by around Rs 66 crore and Rs 44.6 crore.

The report for 2006 further reveals the bank had not made 100 per cent provisioning even for loans classified as frauds. There have been delays of up to three years in detection of frauds,says the RBI report. For the quarter ended December 31, 2006, the NPAs estimated to have been understated amount to Rs 1,115.82 crore. If all loans and those accounts where lim its have not been renewed for a period of over six months are taken into account, the total amount of NPAs of UCO Bank may well exceed Rs 2,500 crore for the financial year ending March 31,2007.According to RBI guidelines, an asset is classified as NPA if it has remained unpaid for over 90 days.

The understatement of NPAs that has been found to have continued for years now is neither accidental nor due to any oversight, but is the result of a well-planned strategy of UCO Bank officials at senior and senior middle levels allegedly with the connivance of the CMD and ED of the bank.As a result of the performance-based incentive scheme of the Government of India, such concealment directly benefits the CMD and ED by overstating the profit of the bank for the relevant financial year.

The bank understated its NPAs even in the prospectus issued at the time of its IPO – which makes those who authorized the issue of such a prospectus liable for prosecution

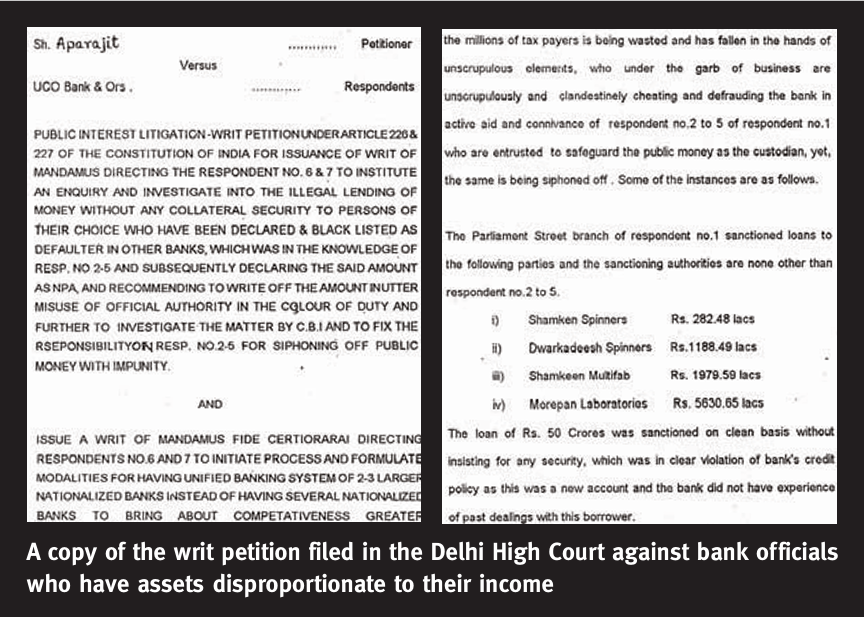

The bank understated its NPAs even in the prospectus issued at the time of its IPO – an act amounting to misstate ment in the prospectus which makes the director and all those who authorized the issue of such a prospectus liable for civil and criminal prosecution under the Indian Companies Act. gfiles is in possession of documentary evidence against various senior officials of the bank who disbursed huge loans without seeking collateral – and to borrowers who were blacklisted and declared defaulters by other nationalized banks.We also have evidence against some officials who have accumulated wealth disproportionate to their known sources of income. A writ petition is also pending with the Delhi High Court on this matter.

A K Gupta, General Manager, Strategic Planning of the bank, while responding to queries, expressed his inability to comment on these issues,cit ing the confidential nature of the report. He, however denied the allegations and said that the bank was holding floating (surplus) provision of Rs 76 crore as of March 31,2005 In this age of globalization and intense competition, public sector banks are facing the heat due to aggressive posturing of most new-age private sector banks such as ICICI, HDFC and so on.

Many of the public sector banks have, in the recent past, thoroughly revamped their working style and shed flab by writing off NPAs from their books and turning their banks into zero-NPA banks.These banks have been duly rewarded by the markets and this fact has been reflected in their market price.Their market capitalization has multiplied many times in the past two-three years.In the process, stake holders have been immensely rewarded. Yet, UCO Bank officials have been cheating its depositors and its stakeholders, including shareholders, honest employees and others.The government, as a major stakeholder in such banks, is also affected.

{kind=link}