THIS is the story about the six-degrees-of-separation principle. In personal lives, one can link with anyone anywhere in the globe through six links—A knows B, who knows C, who knows D, and so on, until the person G, who is the one that one actually wished to connect with. This rule is what primarily drives the popularity of social networks. The same tenet applies in business, and more so, because such connections to reach the right individual are paramount in corporate affairs to get work done.

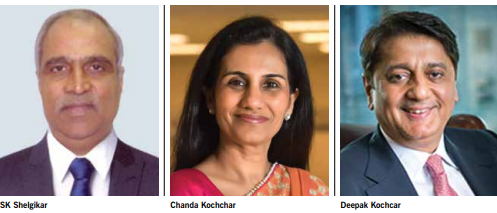

We can start this tale with any person or company mentioned later. But we will start with SK Shelgikar. He worked with the Videocon (Dhoot-promoted) Group for over three decades and retired as its financial advisor in 2013. His name cropped up because of his and Videocon’s dealings with Deepak Kochhar, the husband of Chanda Kochhar, the former head of ICICI Bank, which was accused of extending loans to Videocon as a quid pro quo for the group’s investment in the husband’s firms.

Shelgikar was also associated with CapitaWorld Platform, a private company where the former’s firms had minority stakes. CapitaWorld was a little-known company, which was promoted by a few individuals a few years ago with no experience in financial and technological sectors. Only later did they sell a part of their stakes to Shelgikar’s companies, and a majority stake to SIDBI, the state agency that normally processes loan applications by the small and medium enterprises (SMEs).

Before it sold a substantial holding to SIDBI, CapitaWorld got the technology contract to process and give in-principle clearances to the SMEs that applied for loans under the special scheme, 59-minute loan, announced by Prime Minister Narendra Modi. Since the bid was awarded flouting the tender norms, including the minimum experience required and annual turnover, this hinted that both Shelgikar and the other promoters of CapitaWorld may have political contacts.

While he was with the Videocon Group, Shelgikar became a director in Credential Financial, a firm promoted by Deepak Kochhar. One of Shelgikar’s companies, which invested in CapitaWorld, had a small stake in Credential Finance. Videocon had a sizeable stake in the finance company. The Videocon group invested in another firm, NuPower Renewables, which was promoted by Deepak Kochhar. Supreme Energy, another Videocon Group company, extended a Rs. 640-million loan to NuPower.

Before it sold a substantial holding to SIDBI, CapitaWorld got the technology contract to process and give in-principle clearances to the SMEs that applied for loans under the special scheme, 59-minute loan, announced by Prime Minister Narendra Modi

Later the Videocon Group transferred its stake in Supreme Energy to Mahesh Chandra Pungalia, another advisor to the Videocon Group, who held a minor stake in Kochhar’s Credential Financial. Pungalia’s stake in Supreme Energy was transferred to a trust floated by Deepak Kochhar. Such investments by Videocon in Deepak Kochhar’s firms, and transfer of equity by Videocon to Kochhar, said a whistleblower, was a quid pro quo for a huge loans that Videocon received from ICICI Bank, which was headed by Chanda Kochhar, the wife of Deepak Kochcar.

Such investments by Videocon in Deepak Kochhar’s firms, and transfer of equity by Videocon to Kochhar, said a whistleblower, was a quid pro quo for a huge loans that Videocon received from ICICI Bank, which was headed by Chanda Kochhar, the wife of Deepak Kochcar

Documents filed with the central Ministry of Corporate Affairs showed that NuPower Renewables received Rs. 4-billion equity infusion from DH Renewables, “a fund based in (tax haven) Mauritius which, in turn, was owned by Accion Diversified Strategies Fund of Cayman Islands, a tax haven”. DH Renewables had links with Nishant Kanodia, a businessman based in West Bengal. Kanodia’s Mauritius-based firm, Firstland Holdings, invested a huge sum in Kochhar’s NuPower Renewables between 2010 and 2012. In 2013, it sold the entire holdings to DH Renewables.

Kanodia is the son-in-law of Ravi Ruia who, along with other family members, is the promoter of Essar Group. The Ruias have extended huge loans to Kanodia’s Matix Group, which has set up a huge fertilizer plant in West Bengal. During the 2010-12 period, when Kanodia’s Firstland Holdings was invested in Kochhar’s NuPower Renewables, the Essar Group received a huge loan from ICICI Bank for their steel venture in Minnesota, US. Income tax officials feel that the Essar Group may have connections with DH Renewables’ parent company, the Cayman Islands-based Accion Diversified Strategies Fund.

Recently, the income-tax department raided several offices of the Kanodia-owned Matix Group across the country, including in West Bengal. The government agency told journalists that it has or will question the Ruias to explore if they have any links to Accion Diversified. The department has also questioned the Dhoots. An official anonymously told a newspaper, “This is part of an ongoing probe into NuPower. We are probing why Firstland Holdings made the investment and exited soon after, and whether this has any connections with any Essar Group company.”

Essar Group, it seems from past events, seems to be politically active. It first sold its ailing Essar Oil to the Russian Kremlin-owned oil major Rosneft. Another Russian Kremlin-owned VTB Group was a partner of Rosneft to takeover the Indian firm. The sale was announced in a grand manner through full page newspaper ads as the shining and biggest example of ‘Make in India’, a scheme that was initiated by Narendra Modi. In effect, it was a distress sale by a group plagued with bad loans.

VTB Group owns a bank, VTB Bank, whose boss is Andrei Kostin. According to a piece in the Independent of the UK, this is how he is described: “Conjure up an image of Russia’s most powerful banker, running an organisation subject to western sanctions and accused in some quarters of being Vladimir Putin’s piggy bank.” In the autumn of 2017, Kostin “shocked investors from the West by addressing guests at a gala dinner of Moscow’s huge international banking conference dressed as Joseph Stalin”.

PUTIN’S links with VTB were further partially-disclosed in the Panama Papers, the thousands of documents accessed by the International Consortium of Investigating Journalists. According to the Independent, “In a similar vein, a VTB subsidiary, RCB, was famously accused by journalists investigating the Panama Papers of mysteriously lending hundreds of millions of dollars to a cellist friend of Putin….” The Paradise Papers, a sequel to Panama Papers, indicated that Wilbur Ross, a former minister of commerce in the US, invested in a shipping business “with links to a Moscow-based company whose shareholders included Putin’s friend and judo partner Gennady Timchenko and son-in-law Kirill Shamalov”.

Gujarat model of profits in 59 minutes

IN November last year, Prime Minister Narendra Modi announ-ced a grandiose, and extremely relevant, loan scheme to help the small and medium enterprises (SMEs). He said that the government will ensure approvals of loans of up to Rs. 10 million from state-owned banks through a digital platform within an hour. The platform was appropriately dubbed www.psbloansin59minutes.com. In its own wisdom, SIDBI (Small Industries Development Bank of India), the nodal official agency for such loans, decided to outsource this work, and floated a tender.

![]()

Flouting key clauses of the tender, the bid was awarded by SIDBI to CapitaWorld Platform, a new company floated by three Gujarati entrepreneurs – Vinod Modha (worked with NBFCs), Jinand Shah (CA and financial analyst), and Aviruk Chakaborty (worked in manufacturing sector). One of the crucial eligibility requirements was that the company be in existence since April 2012. CapitaWorld was set up in 2015. Another stated that the winner should have earned a minimum of Rs. 500 million from management consulting work. CapitaWorld’s annual revenue in 2015-16 was ‘Nil’, and this zero figure rose to Rs. 15,680 in 2016-17.

The winner had to float a new company, whose shareholders would include SIDBI and other state-owned banks. This wasn’t done. CapitaWorld’s shareholding changed only in July 2018, when SIDBI and eight public sector banks acquired 54 per cent stake in it, and that too after the payment a huge premium of Rs. 119.39 per share (face value: Rs. 10). Within three years, the original promoters made a killing by selling a part of their shares. The valuation was based “potential earning capacity”, which came into existence because of the tender floated by SIDBI.

Hence, the state-owned SIDBI chose a digital platform constructed by a private company, whose valuation zoomed from almost-zero to Rs. 420 million within three years, entirely because of the selection. And then the state-owned SIDBI, along with eight other public sector banks purchased shares from the original promoters of the private company at this huge valuation. Public profits were comfortable shifted into private pockets.

More important than that, the original three promoters retained a sizeable equity holding in CapitaWorld Platform, which will ensure them unlimited wealth, in terms of possible dividends and even higher valuations, later. The calculation is simple. The platform charges a fee of 0.35 per cent of the loan amount for each application that it processes. A statistics counter on the website, which is now removed, claimed that the platform had 169,000 registrations, and processed loans worth Rs. 230.58 trillion.

A simple calculation shows that the revenues from these approvals 0151—0.35 per cent of the total figure—would be 825.3 million. Media reports, quoting businessmen, claimed that the revenues could be 50-100 times more if a million SMEs applied for loans through the platform. What is intriguing is that CapitaWorld Platform only gives an “in-principle” approval; the relevant bank can still reject the application. But the processing fee i.e Rs. 1180 is non-refundable. What a safe, comfortable, and cosy business model?

However, Kostin told the Independent that “VTB’s hands are clean”. He said that the Panama Papers found money that belonged to David Cameroon, the former British prime minister, and Ukranian president, Petro Poroschenko. The Paradise Papers found the names of Wilbur Ross and, yes, the Queen of England. “Not a single Russian official” in both the Panama and Paradise Papers, he told the British newspaper. Kostin added that “Russia has no offshores (tax havens)”, and that they “all exist in America, in Britain, (and) in Europe”.

IN India, the VTB Group is active, and has other links to the Essar Group. Together with Numetal, which has links with Rewant Ruia, who is the scion of the Essar Group, VTB Capital has formed a consortium to bid for Essar Steel, another ailing company. In fact, when the Supreme Court raised a few questions about Numetal’s connection with Rewant Ruia, a part of the original promoter family, VTB Capital said that it would bid “solo” for the Indian steelmaker. According to newspaper reports, VTB Capital has “sovereign guarantees of the Russian government” for the bid.

In an interview, a senior manager of VTB Capital, Makran Abboud, said, “Ruias are one of our many Indian clients. We have done the biggest transactions with them. We are kind of business friends, but we are not married to each other. We know Essar Steel because of Ruias. Nobody can deny this.” On why VTB selected Rewant Ruia as a partner, he added, “We selected a person whom we worked with. I am comfortable with him. He is there not because we know him, but we believe he can deliver.”

The Indian government, given that it controls SIDBI, must have had a role to play in the selection of CapitaWorld Platform, which gives clearances under the PM’s 59-minute loan scheme

Lest we forget, one has to mention the circumstantial evidence related to the politics of VTB Group in India. ONGC Videsh, an international arm of the Indian state-owned ONGC, an oil explorer, has a partnership the Russian state-owned Rosneft, which has links with the VTB Group. Both Rosneft and VTB, as we said earlier, have connections with Putin and Kremlin. The ONGC partnership happened around the same time as the sale of Essar Oil. There is no proof that the two mega deals are connected.

However, the Indian government must have had a say in the ONGC-Rosneft deal. The Indian government, given that it controls SIDBI, must have had a role to play in the selection of CapitaWorld Platform, which gives clearances under the PM’s 59-minute loan scheme. Just to remind the readers, Shelgikar may be a minority investor, but he has a key responsibility in CapitaWorld Platform, in which SIDBI now has a majority stake but which was originally promoted by three Gujarati entrepreneurs!

Alam Srinivas is a business journalist with almost four decades of experience and has written for the Times of India, bbc.com, India Today, Outlook, and San Jose Mercury News. He has written Storms in the Sea Wind, IPL and Inside Story, Women of Vision (Nine Business Leaders in Conversation with Alam Srinivas),Cricket Czars: Two Men Who Changed the Gentleman's Game, The Indian Consumer: One Billion Myths, One Billion Realities . He can be reached at editor@gfilesindia.com

{kind=link}