IN economic and commercial parlance, banking is a kind of business different from others. In general terms, it is accepting and safeguarding money owned by other individuals and entities, and then lending out this money in order to earn a profit. Banking institutions, therefore, should judiciously combine two distinctly different functions—one as public trustee and the other as profit-making business entity. At the core of its function is the management of its assets in a prudent and profitable manner.

The way they are managing their assets, India’s public sector banks (PSBs) are failing in both functions. In the event, the Non-Performing Assets (NPAs) of these banks have become the talk of the town. According to the Reserve Bank of India (RBI) estimates, the top 30 loan defaulters alone currently account for one-third of the total gross NPAs of PSBs.

The current debt-burden of just 10 corporate entities amounts to a staggering Rs. 7.8 lakh crore: The Anil Ambani-led Reliance Group — Rs. 1.25 lakh crore; Vedanta Group — Rs. 1.03 lakh crore; Essar Group — Rs. 1.01 lakh crore; Adani Group — Rs. 96,031 crore; Jaypee Group — Rs. 75,163 crore; JSW group — Rs. 58,171 crore; GMR Group — Rs. 47,976 crore; Lanco Group — Rs. 47,102 crore; Videocon Group — Rs. 45,405 crore and GVK Reddy — Rs. 33,933 crore.

Though the Finance Minister has reportedly set aside Rs. 70,000 crore this year to ‘service’ corporate NPAs, it is not known how much of these big-guns’ dues falls in that category. It is because the banks, the RBI and the government are very reluctant to declare the details of the biggest defaulters. They willingly take shelter under Section 45E (1) of the Reserve Bank of India Act, 1934, which stipulates that any credit information contained in any statement submitted by a banking company shall be treated as confidential and shall not be published or otherwise disclosed.

In an order passed in 2011, the Central Information Commission directed the RBI to reveal publicly the names of the top 100 industrialists who defaulted on loan repayments to PSBs with a view to “put pressure on such persons to pay their dues”. The RBI moved the Delhi High Court, seeking quashing of this order on grounds that it went against “the cardinal common law principle of bankers’ duty of confidentiality and against the basic tenets of banking”.

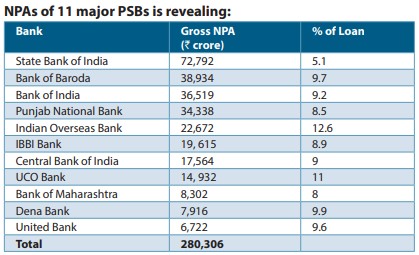

But this ‘common law principle’ does not seem to apply to small defaulters. About four years back, when rumblings of the bad-loan saga were just beginning to surface, some PSBs placed advertisements in daily newspapers with photographs of individual defaulters alongside a stern warning that if they failed to respond, photographs of their guarantors would also be published. SBI, India’s largest bank with NPA of Rs. 72,792 crore, targetted a woman with a petty outstanding loan of Rs. 52,264. Other banks followed suit. But none of them touched the big guns!

THE methods these banks adopt to recover small NPAs far surpass that of the legendary Shylock of The Merchant of Venice. Referring to this phenomenon, RBI Governor Raghuram Rajan had this to say: “Law becomes more draconian in an attempt to force payment. The SARFAESI Act of 2002 is very pro-creditor as it is written….Its full force is felt by the small entrepreneur who does not have the wherewithal to hire expensive lawyers or move the courts, even while the influential promoter once again escapes its rigour. The small entrepreneur’s assets are repossessed quickly and sold, extinguishing many a promising business that could do with a little support from bankers.”

Here is a real-life narrative of a Small Scale Industry (SSI) near Chennai to substantiate what the RBI Governor said. A term loan was received by the company from the Tamil Nadu Industrial Investment Corporation (TIIC). A PSB provided working capital/bill discounting assistance of Rs. 15 lakh in 1988 against the hypothecation of raw materials, stock-in-process and finished goods. As additional security, the bank surreptitiously retained the title deed of the residential house belonging to the guarantor.

The methods banks adopt to recover small NPAs far surpass that of the legendary Shylock of The Merchant of Venice. Referring to this phenomenon, RBI Governor Raghuram Rajan had this to say: “Law becomes more draconian in an attempt to force payment…”

The fully set up factory commenced production in February 1989 as captive unit of a large industry manufacturing commercial vehicles and engines and a major supplier to Defence Forces. However, the captive business of about Rs. 50 lakh per annum unexpectedly collapsed due to severe budgetary cuts imposed in the Defence Ministry. The PSB was immediately put on notice and proposal for diversifying manufacturing activity was submitted with request to enhance working capital limits. Had those proposals been sanctioned, the SSI would have diversified the product range, marketed the products and become viable and profitable. No support whatsoever came and the SSI folded up.

After killing the SSI, in September 1998, the PSB filed an application in the Debt Recovery Tribunal (DRT) under the Recovery of Debts Due to Banks and Financial Institutions, 1990 (RDDBFI Act), claiming a sum of Rs. 97,33,574, and seeking its recovery by attaching and selling the residential house. This property was coveted by a certain senior bank official, who had expressed it openly.

So, when the RBI issued guidelines on July 27, 2000, for One Time Settlement (OTS) of dues from SSIs, this PSB was not really interested in complying with it. After several letters, the bank intimated an arbitrary figure of Rs. 38.68 lakh. On its review by a special recovery group, comprising two General Managers and a Zonal Manager in December 2001, dues were brought down to the correct amount of Rs. 20.05 lakh as per RBI’s OTS norms; Rs. 5 lakh was immediately paid as down payment with a request for early confirmation. The confirmation never came because senior bank managers were not propitiated with bribes!

THE PSB turned Shylock on September 25, 2004, and issued a notice under Section 13 (2) of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (SARFAESI Act), claiming a massive sum of Rs. 3.27 crore as dues to be paid within 60 days. The bank got the residential house attached, put up a notice of possession and another for ‘Tender Sale’, naming and shaming the entrepreneur. Prospective bidders went and inspected the house. The Debts Recovery Tribunal (DRT) prevented this foul game in time by issuing a stay order. On December 20, 2006, the Tribunal quashed all coercive actions of the bank under SARFAESI Act as invalid and illegal.

Bankers are seeking more arbitrary powers that cannot be challenged. They are already the prosecutor, jury and judge as far as the borrowers are concerned. Now they want to be executioners as well

On August 3, 2007, DRT passed final orders on the PSB’s application to determine the dues. Despite ‘discovery of documents’ ordered by the DRT, the bank concealed the settlement at Rs. 20.05 lakh. Even the oft-repeated settlement at Rs. 38.68 lakh was denied by the PSB. But DRT had proof and, therefore, decreed this amount as due with PLR of interest at 8 per cent, recording the undertaking given by the bank’s counsel. The entrepreneur deposited Rs. 51.14 lakh in DRT. This should have given a quietus to the whole matter, allowing the entrepreneur to breathe easy.

Not to be. After immediately appropriating the full amount, the PSB went on appeal before the Debts Recovery Appellate Tribunal (DRAT), Chennai, with all kinds of falsehood, intentionally giving the wrong address for service to the entrepreneur. The bank retracted from the undertaking given by its counsel before the DRT. The Appellate Tribunal set aside the DRT order on January 28, 2009, by relying on a totally irrelevant Supreme Court judgment. The copy of this order was released after four months, just a day before the Presiding Officer retired. Immediately thereafter, the Bank moved application before the DRT for a Recovery Certificate for the full amount with further interest and costs, that is Rs. 16,849,192. Behind the back of the borrower, the DRT issued Recovery Certificate for this amount.

The DRT’s RO immediately issued Demand Notice for the amount on July 7, 2009, summoning the entrepreneur on July 24, 2009, at 11.30 am to initiate the recovery procedure. Fortuitously, a writ pettion in the Madras High Court, against the DRAT order, came up for hearing on the same date and a stay was obtained at 11 am. Shylock sought revenge by activating the SARFAESI notice of May 7, 2007, claiming Rs. 5.07 crore as dues and appointed an ‘Authorised Officer’ to take possession of and sell the residential house.

This would have happened but for the HC rendering its judgment, setting aside the DRAT order and castigating the bank and its officials. The HC’s Order Copy was released on April 9, 2010. The 90-day limitation for PSB to file a special leave petition (SLP) in the Supreme Court expired on July 8, 2010. The HC order was clear and there was no scope for any appeal. The senior counsels of the bank had given their opinion against filing an SLP. But the bank’s senior managers overruled these opinions and filed an SLP after a delay of 24 days.

Despite this grievous flaw, the SC condoned the delay, entertained the SLP and issued a notice to the entrepreneur. After 12 listings, 28 adjournments and over four years of anguish, SLP was finally disposed of by the SC on October 14, 2014, with a crisp two-line order: “Heard learned counsel for the parties and perused the relevant material. We do not find any legal and valid ground for interference. The Special Leave Petition is dismissed.” Thus came the closure of the case after nearly two decades of hostile and frivolous litigation by the PSB. Perjury was the bank’s practice in the tribunals, High Court and the Supreme Court. All this happened with the full knowledge and connivance of senior managers, including a former CMD.

Under the Banking Regulation Act, the RBI can intervene and remedy the situation. But this is only on paper. Desperate and repeated pleadings to the RBI Governor fell on deaf ears. Responses from the Ministry of Finance and Chief Vigilance Commissioner were no different.

There are far worse victims of PSBs than this entrepreneur. India’s modern-day Shylocks have far exceeded this character in greed, cruelty and deceit. They not only want a pound of flesh, but also the blood that flows. This carnal demand is made on small entrepreneurs who had staked everything to establish a business and live in dignity. These Shylocks do not care a damn if the person who had borrowed the money or had stood guarantee lose all dignity and perish in the process. For they have the laws, the State and the judicial system to propitiate, protect and pamper them.

Let us see how this happens. When an entity or an individual borrows money from the bank and delays repaying the borrowed money, banks classify them as defaulters and initiate actions for recovery of loans. The special enactments empowering banks and financial institutions to proceed against the defaulters are the RDDBFI Act and SARFAESI Act.

THESE were enacted to facilitate easy recovery of loans due to banks, the former with the help of adjudicating authorities and the latter an arbitrary suo motu procedure with powers to attach collateral/mortgaged properties and sell them. These are co-existing remedies, meaning banks can resort to both at the same time. This is where there is huge corruption by bank managers. Most of the genuine commercial/residential properties mortgaged to the banks become high-value over time. SARFAESI gives sweeping powers to bank managers to summarily take possession of these properties once a loan is declared NPA. If the borrower bribes the bank managers heavily, they allegedly settle the dues without charging interest on the borrowed amount and release the property. If not, the properties are sold through brokers at prices much below market rates and the booty is shared. The hapless borrower, deprived of livelihood, is thrown on the streets. It is largely with this view that NPAs are ‘manufactured’ for truly secured loans.

A more insidious method of corruption is to sanction huge loans without proper due diligence and accept fake or low-quality properties as security. Though counted as ‘secured’, these are actually unsecured loans. It is in these loans that large default takes place and invoking the SARFAESI Act is of no use to the banks. So, they move the DRT under the RDDBFI Act so that banks can hunt for properties of the borrower and his family not given as collateral. This is a cumbersome process, consuming years of litigation and counter-litigation. In the meanwhile, NPAs keep mounting and skyrocketing as is happening now.

Despite draconian powers under the SARFAESI Act and vast powers under the RDDBFI Act, banks are unable to prevent NPAs or recover them quickly largely because of inefficiency, corruption or political skullduggery. Tribunals and courts, where the bank’s actions are challenged, are not always obliging. Bankers want this impediment to be removed and are seeking more arbitrary powers. They are already the prosecutor, jury and judge as far as borrowers are concerned. Now they want to be executioners as well. Despite its Governor blowing hot and cold, RBI is yielding. Its December 2014 guidelines allow banks to classify any defaulting borrower as non-cooperative and then a wilful defaulter.

A more insidious method of corruption is to sanction huge loans without proper due diligence and accept fake or low-quality properties as security. Though counted as ‘secured’, these are actually unsecured loans

A non-cooperative borrower “is one who does not engage constructively with his lender by defaulting in timely repayment of dues while having ability to pay, thwarting lenders’ efforts for recovery of their dues by not providing necessary information sought, denying access to assets financed/collateral securities, obstructing sale of securities, etc. In effect, a non-cooperative borrower is a defaulter who deliberately stonewalls legitimate efforts of the lenders to recover their dues.”

The definition encompasses all borrowers within its scope and leaves very little room for them to raise a voice or stand up for rights. Any legitimate attempt to do so or any attempt not to succumb to the demands of the banks would lead to a borrower being classified as non-cooperative and then being declared a ‘willful defaulter’. Following up, the RBI in January 2015 revised its willful defaulter guidelines, which not only notifies a borrower as “willful”, but also declares him a defaulter for life. Going a step further, the Securities and Exchange Board of India (SEBI) has proposed to completely bar willful defaulters from any access to equity and debt markets.

THE scenario is such that the SARFAESI Act, a subordinated legislation devoid of natural justice, will now be the rule of law with respect to defaulters. For example, if the bank resorts to action under Section 13(4) of SARFAESI, appealing against it would make the borrower ‘non–cooperative’. Thus, it not only empowers the bank to decide upon the fate of the borrower, but also denies him the right to appeal. Once classified as non-cooperative, it is just a matter of time to classify him as a willful defaulter; and once a willful defaulter, what awaits him is banishment for a lifetime, completely choking all avenues of financial assistance.

With these harsh regulations on loan recovery and NPAs, the new mantra seems to be “the bank is always right”. Gone are the days of customer-friendly banking. Now a borrower will have to obey what his banker says else his fate is sealed! Tragically, because of rank crony capitalism being practised by the government and its instruments, it is the small fry who face the gallows while the big whales keep laughing all the way to their banks!

These banks are the axis of the ‘Make in India’ juggernaut propelled by the big whales. Ideal ground for ‘Banker’s Heist’ promoted by the UPA and now perpetrated by the NDA!

The writer is a former Army and IAS officer. Email: deva1940@gmail.com

IAS (retd) with a distinguished career of 40 years - worked in Army, Govt, Private, Politics & NGOs.

{kind=link}