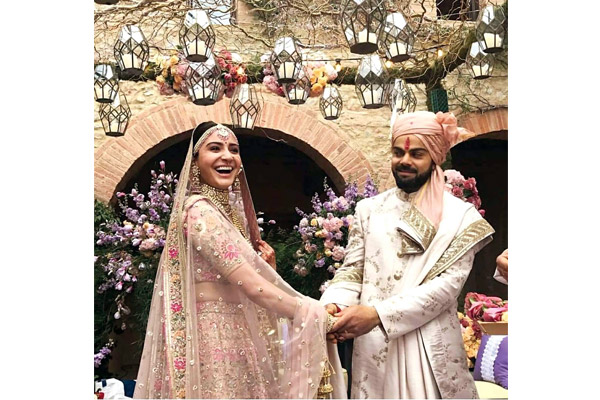

REPORTS in the media surface occasionally about social functions like marriages, birthdays, anniversaries, etc., being performed on sea/air and at reputed places in splendid way with great pomp involving substantial expenses. The common man is both amused and aghast in knowing about the same. The latest in the series is marriage of Anushka Sharma with Virat Kohli – both Indian celebrities. In spite of both being Indian citizens, they have preferred to have the marriage performed at an Italian countryside resort named Borgo Finocchieto in the province of Siena in Central Tuscany, which is said to have the most expensive holiday properties in the world – second on Forbes list of 20 most expensive holiday destinations, where rates range from Rs. 6,50,000 to Rs. 14 lakh per night. The marriage is said to have been attended by 42 to 45 close friends and relatives and was followed by receptions at Delhi and Mumbai. In the past also, marriages have been performed in grand ways.

Looking back to name a few one gets reminded of (late) Jayalalitha’s foster son’s marriage at Chennai, a marriage at Mumbai, where the entire Wankhede stadium was booked and vastly decorated; the marriage of two members of Sahara family at Lucknow and recently the marriage of the daughter of a mining baron at Hyderabad. Besides expenses on the functions, costly presents are also exchanged. The trend is on the upswing.

I hasten to clarify that while mentioning such events, I do not wish to suggest that expenses on such functions have not been or will not be met from known sources of income and that each citizen of the country is free to arrange his/her personal affairs the way they like within the framework of law. But in exercising rights, one has to keep in mind the sensitivities of others also. The Constitution of India too prescribes duties along with rights. Also, as a citizen of the country, I do feel that it is not good to spend money in this way on unproductive channels and incur expenses in foreign exchange abroad when India itself has beautiful spots of its own.

Coming to the title of the subject, such expenditure needs scrutiny even if the same is explained in the same manner as Income Tax returns are checked. The I.T. Act vide Section 133A provides strong background for this. Sub-section (5) of the section specifically deals with surveys concerning such functions. Enquiries can be made regarding these after the event and concerned persons’ statements recorded during enquiries.

Section 133A also provides safeguard to the effect that no cash found during the survey can be seized or removed. Proceedings in this context mean a completed, pending or proceeding to be commenced in future. During survey, if a person refuses to comply by not producing account books/documents or give statement, action under Section 131 of the I.T. Act can be taken to enforce compliance. Thus, the powers are sufficient to get the requisite response. What is needed is effective use of the same with proper planning and without hurting the sentiments of the assessees.

As Commissioner of Income Tax years back, I could detect use of unaccounted money in such functions, imposing tax on such money with proper planning.

The success of the operations depends on proper homework. The first step necessary is to gather intelligence about the function, i.e. date, time, venue, duration, and so on. Attempt should be to back any decisions with photographs of decorations, settings, lighting, food serving arrangements in the shape of stalls, etc. Then the next step is to swing into action immediately after the function, ceremony or event. The survey party needs to station itself at a place close to the venue and start enquiries after the conclusion of the function, say in cases of marriages after the departure of the bride and marriage party.

Generally, attempts have been to support high expenditure on the functions by the cash gifts claimed to have been received during functions; this can be blunted by getting the cash counted and the statements of the person(s) in-charge of the same recorded. Simultaneously, enquires about costs of catering, providing shamianas, chairs and sofas, electrical lighting, conveyance charges, hire charges for the venue, other gifts received, etc., can also be made and the statements of the concerned persons recorded. All these need to be done swiftly after the function and not after a year or more, waiting for the returns of income to be filed. Time is of the essence in such cases. Delays provide opportunities to create evidence to support the expenditure.

Where marriages are performed outside India, statements of the concerned persons need to be recorded regarding expenditure, say within two weeks of the marriage. Also, the Indian missions in other countries can be sounded to collect the information through exchange of information agreements in fast manner from countries with whom India has such agreements. A clause can also be inserted in Section 285BA of the I.T. Act, which places obligations on taxpayers to furnish statements of financial transactions, etc., on pain of penalty under Section 271FAA of the I.T. Act. The limit for reporting could be fixed at Rs. 5 lakh for marriages and Rs. 2 lakh for other functions in the manner, to be prescribed under the Rules within 15 days of the conclusion of the function or the event. Also, stringent punishments by way of prosecution for those, whose affairs are found to be not clean, need to be prescribed to create deterrence with stipulations that such cases will be dealt with in fast track courts and the names of the persons found guilty will be published with details about unaccounted money used in such functions.

REGRETFULLY, it is noticed that the I.T. Department’s response to such situations has lacked strong will and timely actions because of which desired results have not been achieved despite the fact that such expenses are continuing unabated in many cases, using unaccounted money–throwing a challenge to the I.T. Department that we will continue in this manner, check if you can.

Such unproductive wasteful expenditure also gives a negative picture of the functioning of the Government, besides causing loss of revenue, waste of food and other resources in a country, where nearly one-third population lives below the poverty line and where a large section is not able to manage even two-course meals a day. The I.T. Department needs to wake up from its slumber and scrutinise such ostentatious expenditure effectively.

The writer is former Chairman, CBDT

{kind=link}