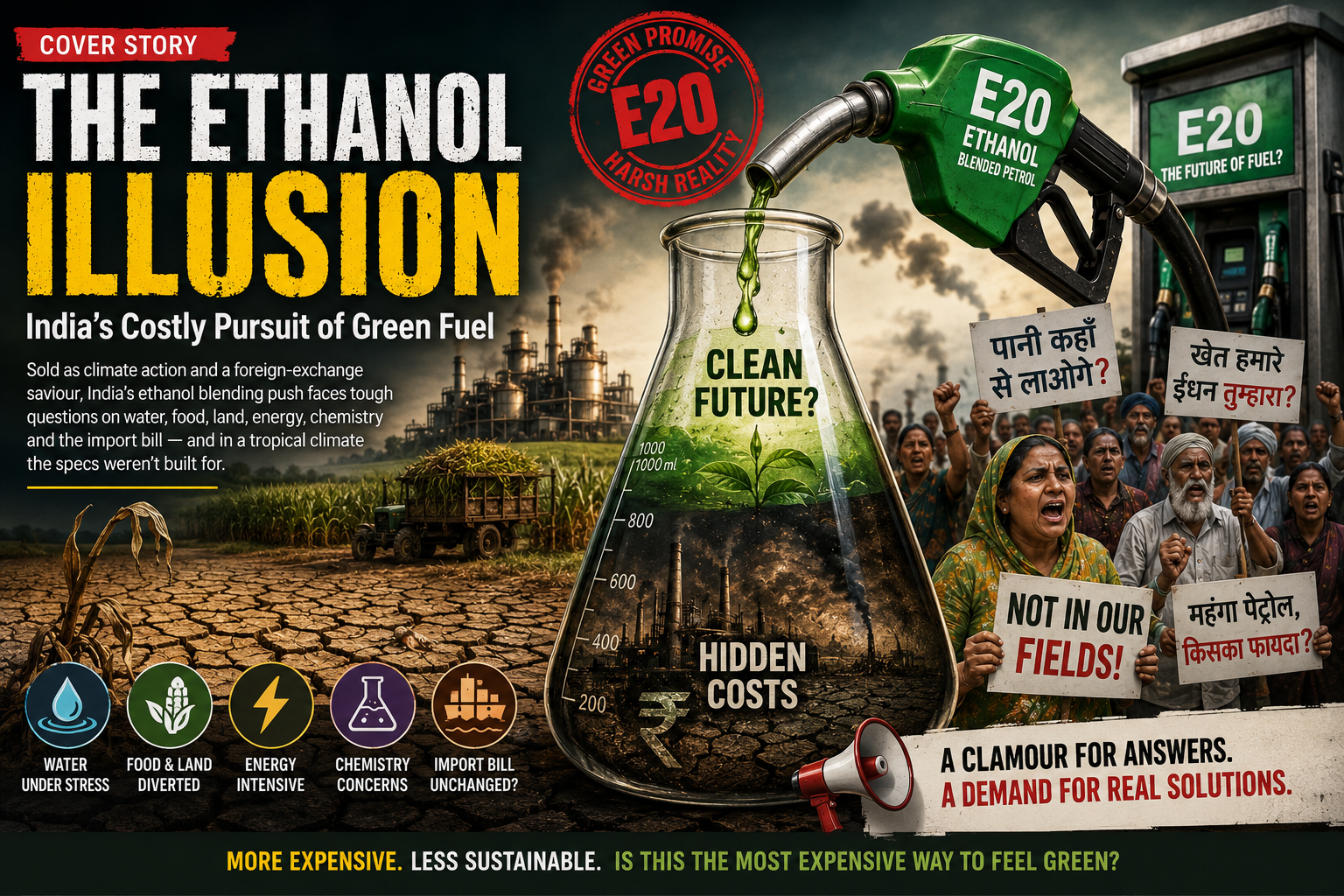

The Green Mirage of Ethanol Blending

India’s ethanol blending programme is sold as climate action and a foreign-exchange saviour. A closer look at the water, land, food, energy, chemistry and import-bill ledger — and at a tropical climate the programme’s specifications weren’t built for — suggests it may be one of the country’s more expensive and environmentally unfriendly ways of feeling green.

In December 2025, public sector oil companies announced that petrol sold across India now carries 20 per cent ethanol. This is the E20 target, reached five years ahead of the original 2030 deadline set under the National Policy on Biofuels. Blending has risen from roughly 1.5 per cent in 2013-14 to 20 per cent today — a thirteen-fold jump in just over a decade.

Union ministers have called ethanol the fuel of the future. In July 2026, the Ministry of Petroleum and Natural Gas issued a ten-point rebuttal of what it labelled misinformation — on engine damage, water use, insects in fuel tanks, and environmental risk. It insisted the programme rests on scientific evidence and global practice.

Buried inside that defence is an admission worth pausing on. Asked about water, the ministry pointed to environmental clearances and Zero Liquid Discharge norms at ethanol distilleries. It did not address the water, energy and chemistry consumed upstream, in the fields, long before any crop reaches a distillery gate.

The real story of this programme’s environmental cost lies not in the factory, but in the farm; not in the tailpipe, but in the aquifer and the fuel tank of the tractor that ploughed the field.

Fig. 1 — The visible savings on one side, the uncounted ledger on the other.

World Ethanol Map: Everyone Else Stopped at 10%

Fig. 2 — Blending ceilings by country/bloc. Source: EPA; EU member-state fuel reporting; Australia, Vietnam, China blending rules; Brazil ANP.

India’s E20 is not simply catching up to a global norm — it is overshooting one. The overwhelming majority of countries that blend ethanol into petrol cap it at 10 per cent. In the United States, despite a July 2026 EPA waiver permitting summer sales of E15, more than 95 per cent of pump sales remain E10.

Vehicles from before 2001 are not approved for anything higher, so the effective US ceiling has stayed near 10 per cent for over a decade. Across the European Union, E10 is standard in only 19 of 27 member states. Much of southern and Mediterranean Europe — Spain, Portugal, Italy, Slovenia, Croatia, Greece — still runs largely on E5.

Sweden actually cut its blending mandate from 7.8 per cent to 6 per cent between 2023 and 2026. Australia caps ethanol content by law at 10 per cent nationally, Vietnam mandates just 5 per cent, and China has pulled back from its early national E10 ambitions.

Fig. 3 — Brazil’s five-decade build-out vs. India’s five-year sprint. Source: Brazil ANP ethanol mandate history; India Ministry of Petroleum & Natural Gas, PIB.

The conspicuous outlier is Brazil, which runs E18 to E30 — raised to a mandatory 30 per cent as recently as mid-2025 — and permits pure hydrous ethanol, E100, for flex-fuel vehicles. But Brazil’s high blend was not a five-year sprint bolted onto an unmodified fleet. It is the product of nearly five decades of parallel investment, beginning with mandatory blending in 1976.

Flex-fuel engineering was developed through the 1980s and 1990s specifically to run reliably on high ethanol content. The vehicle fleet, fuel-line materials and retail infrastructure were built and retrofitted in step with the rising blend ratio, not after it.

India reached E20 in five years flat, asking a vehicle fleet still overwhelmingly built for E0 or E5 to absorb, in under a decade, a blend ratio double the ceiling most of the ethanol-using world has settled on.

Give the Programme Its Due, Before the Bills Arrive

Fig. 4 — What E20 delivers on its own preferred metrics. Source: Ministry of Petroleum & Natural Gas; NITI Aayog; Reuters (independent CO2 estimate).

It would be dishonest to start anywhere but with what the programme has actually delivered. Government data credits the Ethanol Blended Petrol programme with substantial foreign exchange savings on crude imports and payments running into lakhs of crores routed to farmers as assured offtake for sugarcane, maize and surplus rice.

The ministry places the decade’s avoided CO2 emissions at roughly 930 lakh metric tonnes, though independent estimates cited by international newswires put the figure closer to 54 million tonnes. Even the headline climate number, in other words, depends on whose accounting method is used.

A NITI Aayog study is cited as finding that sugarcane-based ethanol cuts greenhouse gas emissions by around 65 per cent and maize-based ethanol by around 50 per cent relative to petrol, on a per-litre combustion basis. None of this is fiction.

The question this piece asks is narrower and less comfortable: what does the ledger look like once the inputs — water, land, food, and the energy spent producing the fuel itself — are added back in, rather than left off the page because they are harder to price than a barrel of crude?

The Litres Behind the Litre

Fig. 5 — Water consumed per litre of ethanol, by feedstock. Source: India food secretary, 2026 press briefing; NITI Aayog ethanol roadmap.

Start with water, because it is the input the government has fought hardest to minimise in public. A widely circulated claim that ethanol production consumes 10,000 litres of water per litre of fuel was dismissed by the ministry as baseless.

The number is not, in fact, invented. It traces to India’s food secretary, who told reporters that rice-based ethanol requires approximately 10,790 litres of water per litre once cultivation irrigation is included.

Maize, by the same reckoning, requires roughly 4,670 litres, and sugarcane — the feedstock the programme still leans on most heavily — consumes about 3,630 to 3,636 litres per litre of ethanol produced. A NITI Aayog roadmap document puts cane cultivation water use at 1,600 to 2,100 litres per kilogram of sugar.

“India’s ethanol expansion plan has focused heavily on scaling first-generation production in regions such as Maharashtra, where groundwater depletion is already a concern.” — Prof. Anjal Prakash, FLAME University, IPCC author

Fig. 6 — Ethanol capacity by state vs. groundwater stress. Source: Ministry of Petroleum & Natural Gas; Central Ground Water Board.

The geography compounds arithmetic. India’s total ethanol production capacity stands at roughly 1,822 crore litres, concentrated precisely where water is scarcest rather than evenly spread across the country.

Maharashtra alone hosts close to 396 crore litres of capacity, even as its Vidarbha and Marathwada regions report chronic drinking-water shortages. Uttar Pradesh and Karnataka, the other two major producing states, draw from groundwater reserves the Central Ground Water Board has independently flagged as critically depleted.

Distilleries cluster in cane-growing belts for logistical convenience — proximity to feedstock, existing mill infrastructure. That means the industry’s siting logic and India’s water-stress map point in exactly the wrong direction relative to each other.

NITI Aayog’s own Composite Water Management Index has warned that groundwater in 21 major Indian cities could approach zero by 2030. Ethanol expansion is proceeding, for now, without a basin-level water budget that would tell a distillery in Solapur or Bijnor whether the aquifer beneath it can bear the load.

Fuel, Feed and Food Fight for the Same Acre

Fig. 7 — Maize diverted to ethanol, 2022-23 to 2024-25. Source: Economic Survey of India 2025-26; USDA FAS GAIN Biofuels Annual, India.

Water is only the first constraint. The second is land — and what that land was growing before ethanol policy made a different crop more profitable.

Maize is the clearest case study. Ethanol’s maize demand rose from roughly 0.8 million tonnes in 2022-23 to 12.7 million tonnes by 2024-25, a fifteen-fold jump in two years, driven by an administered price that climbed at over 11 per cent annually along with an assured government offtake.

Farmers responded exactly as the incentive intended. Maize acreage in the 2025-26 kharif season expanded by roughly nine lakh hectares, and the Economic Survey 2025-26 itself noted that this land came substantially at the expense of pulses and oilseeds — two categories where India already runs chronic import deficits.

The knock-on effects reach the dinner table faster than most energy-policy debates do. Poultry and dairy feed depend on maize for 60 to 70 per cent of their composition.

As ethanol distilleries began competing for the same grain, India — a country that has historically exported maize — imported it in 2024 at volumes reported to be nearly eighty times higher than the year before. Small poultry farmers in states like Uttar Pradesh have described feed costs rising by as much as 40 per cent.

A squeeze in maize supply is ultimately passed on in the price of eggs, chicken and milk — protein sources that lower-income households rely on most.

Distillers’ grain byproduct, DDGS, is offered as a partial substitute for feed and soybean meal, but industry assessments treat it as a partial offset at best. Its growing use has ironically begun depressing domestic soybean prices even as India continues importing 60 to 70 per cent of its edible oil requirement.

One estimate of what meeting the 2025-26 target actually requires in physical terms: roughly 275 million tonnes of sugarcane, 6.1 million tonnes of maize and 5.5 million tonnes of rice, drawing on as much as seven million hectares of cropland. A separate analysis by a Delhi-based think tank calculated that hitting the 20 per cent target diverts land equivalent to roughly seven times the built-up area of New York City.

Land, unlike a subsidy line, cannot be reallocated back to pulses the following season without a multi-year lag. Cropping patterns, once shifted by a price signal, are sticky.

Beyond Ethanol: What Else That Acre Could Grow

Fig. 18 — Foreign exchange earned per hectare, cereal/feed crops vs. fruit exports. Source: FAO assessment of India’s tropical fruit trade.

The “it helps farmers” case for ethanol feedstock only holds up against doing nothing. It says nothing about whether the same acre, the same water and the same farmer could earn more — for the household and for the country’s import bill — growing something else entirely.

Start with the most direct substitution. The Economic Survey 2025-26 has already confirmed that maize acreage expanded into land that would otherwise have grown pulses and oilseeds — precisely the two categories India pays the most to import.

India’s edible oil import bill exceeded $15 billion in 2023-24 and kept climbing; the bill for just the first half of 2025-26 ran 19 per cent higher than the year before, at roughly Rs 87,000 crore. Pulses added a further $5.5 billion in 2024-25 imports, a record.

Every hectare shifted back to mustard, groundnut, soyabean, tur or moong works against both of those numbers at once. It does not just displace crude oil imports the way ethanol claims to — it displaces edible-oil and protein imports directly, at the plate rather than the pump.

The same price incentive pulling land toward ethanol feedstock is pulling it away from the two import categories India can least afford to keep growing.

Annual row crops are not the only alternative, either. Fruit trees ask for real investment and care in their first two to three years, and comparatively little afterwards, for a productive life that can run for decades.

Guava makes this case rather than complicating it. Far from becoming an import story, India has turned it into a horticulture success — guava exports have grown 260 per cent since 2013 and fetched over $154 million in 2023 alone, from orchards that need a fraction of cane or maize’s water and fertiliser once established.

The broader export economics are striking. Fruit exports typically earn 20 to 30 times more foreign exchange per hectare than cereal crops do, according to FAO’s (Food and Agriculture Organisation) assessment of India’s tropical fruit trade — a gap ethanol’s crude-oil-substitution math does not come close to closing.

None of this requires abandoning the acre to a single crop, either. The understory of a mature orchard — the space between and beneath the trees — can carry creeper vegetables and leafy greens, adding a second income stream and a second nutritional one from land that would otherwise sit bare between harvests.

There is a soil argument too, and it points the same direction. Perennial tree roots hold soil structure together year-round in a way annually, heavily tilled row crops like cane and maize do not, reducing erosion on exactly the land this piece has already flagged as water-stressed.

None of this is a case against farmers earning from ethanol feedstock while the programme exists — it is a case that “farmers benefit” was never a complete argument on its own. Measured against pulses, oilseeds and fruit, the same acre could be doing more for the farmer, the import bill and the soil than a litre of ethanol ever will.

Carbon Accounting: The Tailpipe vs. the Tractor

Fig. 8 — What tailpipe-only accounting leaves out. Source: NITI Aayog ethanol GHG study; international biofuel lifecycle-assessment literature.

Even the climate case, the programme’s central justification, is less settled than the headline emissions-avoided figures suggest. The NITI Aayog estimate of a 50 to 65 per cent lifecycle emissions reduction is a per-litre combustion comparison against petrol.

It does not fully net out the fertiliser-intensive cultivation of sugarcane and maize, the diesel used in irrigation pumping and harvest transport, or the land-use change where pulses and oilseed acreage is displaced elsewhere. International biofuel literature has long flagged this as the core weakness of first-generation, food-crop-based ethanol.

Gains calculated purely at the tailpipe can be substantially eroded, or in some scenarios reversed, once cultivation-stage emissions and indirect land-use change are priced in. India’s own policy documents acknowledge this in principle by prioritising eventual movement to second-generation ethanol made from agricultural residue rather than food grain.

In practice, 2G capacity remains only a small share of the programme. The roadmap toward E85 and E100 flex-fuel vehicles, for which the Ministry of Road Transport issued a draft notification in April 2026, would increase dependence on first-generation feedstock well before second-generation capacity is ready to fill the gap.

2G Ethanol: The Promise Still Stuck in Neutral

Fig. 9 — 2G ethanol’s real scale against national requirement (log scale). Source: Indian Oil Panipat plant specs; PM JI-VAN Yojana approvals; National Policy on Biofuels.

The government’s standard answer to nearly every argument in this piece is the same one: wait for second-generation, or 2G, ethanol. Made from agricultural residue — rice straw, wheat straw, corn cobs and stover, cotton stalk, sugarcane bagasse — 2G genuinely sidesteps the food-versus-fuel argument, since the feedstock is waste that would otherwise often be burned in the field.

India is not short of raw material. The country generates somewhere between 230 and 600 million tonnes of crop residue a year, depending on the estimate used, and Punjab and Haryana alone produce over 35 million tonnes of rice straw annually.

On paper, converting a fraction of that residue — together with grain that has genuinely spoiled in storage — into fuel looks like the cleanest possible answer to almost every objection raised above. The trouble is scale, and it is worth being precise about how large the gap still is.

India’s flagship 2G facility, Indian Oil’s plant in Panipat, Haryana, is designed to process rice straw into 100 kilolitres of ethanol a day. Government-linked assessments note it has consistently operated below that design capacity since launch, hit by the variable quality of agricultural waste damaging downstream processing equipment.

Bharat Petroleum’s Bargarh plant in Odisha and Hindustan Petroleum’s Bathinda plant in Punjab are built to similar scale. Under the government’s Pradhan Mantri JI-VAN Yojana scheme, only six commercial and four demonstration 2G plants have been approved nationally, backed by roughly Rs 1,800 crore in funding.

Even at full design capacity, a handful of 100-kilolitre-a-day plants add up to a few crore litres a year — a rounding error against a national ethanol requirement running into thousands of crore litres at E20.

The National Policy on Biofuels itself targets only 500 to 1,000 crore litres of cellulosic ethanol annually by 2030. Second-generation ethanol is not yet the escape hatch it is invoked as; it is closer to a demonstration technology still being debugged at commercial scale.

The Chemical Combat Behind Crop Waste

Fig. 10 — Every pretreatment step has a waste stream attached. Original process-flow illustration based on standard lignocellulosic pretreatment chemistry.

Even setting scale aside, 2G ethanol is not the environmentally costless process its promoters sometimes imply. Turning fibrous crop waste into fermentable sugar is intrinsically harder than fermenting the starch already sitting inside a grain of maize.

Lignocellulosic biomass is built from cellulose, hemicellulose and lignin bound tightly together, precisely so the plant’s structure resists breakdown. A 2G plant has to do chemically and mechanically what a 1G distillery gets largely for free from a food crop’s own chemistry.

The process runs in sequence: raw straw or cob is mechanically shredded into fine, uniform particles, an electricity-intensive step at commercial tonnages. It is then chemically pretreated, commonly with dilute sulphuric acid under sustained heat and pressure, to loosen the lignin and expose the cellulose and hemicellulose inside.

Enzymes — themselves manufactured products with their own energy and industrial footprints are used to hydrolyse that material into fermentable sugars. Fermentation and distillation follow, both requiring sustained thermal energy exactly as in a 1G distillery.

Every one of those additional steps has a waste stream attached. Acid pretreatment generates a hot, chemically loaded process liquor carrying dissolved lignin fragments and inhibitory compounds such as furfural, and this wastewater carries a heavy organic load that must be treated before discharge.

Where the acid is neutralised with lime, the reaction produces a solid gypsum-like residue that requires disposal. The leftover lignin-rich solid fraction can, to be fair, often be burned to power the plant’s own boilers — a genuine partial offset, similar in spirit to bagasse cogeneration in a sugar mill — but burning it also generates its own particulate and combustion emissions.

2G ethanol trades one set of environmental costs — the cultivation-stage water and land burden of food-crop ethanol — for a different set concentrated at the processing stage, rather than eliminating environmental cost altogether.

There is a further, more mundane cost: collection logistics. Agricultural residue is scattered across thousands of small holdings, seasonal, and bulky relative to its energy content, which is why viable 2G projects depend on collection networks spanning 50 to 100 kilometres.

That gathering runs on diesel-powered transport, farm by farm, considerably less efficient per tonne delivered than trucking cane from a concentrated growing belt to an adjoining mill. A peer-reviewed study specifically modelling wheat-straw ethanol in Indian conditions flags exactly this collection and storage loss as a source of energy variation between plants.

None of this argues against pursuing second-generation ethanol — diverting stubble that would otherwise be burned is close to an unambiguous air-quality good, regardless of how the energy arithmetic nets out. But it is an argument against treating 2G as a free pass that makes the concerns raised earlier in this piece moot.

EROEI: Spending a Rupee to Save a Paisa?

Fig. 11 — Net energy return by feedstock. Source: Pimentel & Patzek; USDA-linked corn-ethanol studies; Hiloidhari et al. 2021; Brazil ethanol EROEI literature.

There is a more fundamental question sitting underneath the water and land arguments: does the programme return more usable energy than it consumes to produce, once every stage from seed to petrol pump is counted? This is the domain of net energy analysis, or EROEI — energy returned on energy invested.

It is a separate test from the carbon accounting discussed above. A fuel can look reasonable on a tailpipe-emissions basis and still be a poor energy investment if the cultivation-to-distribution chain behind it consumes nearly as much energy as the fuel eventually delivers.

Picture the actual chain. Diesel-run tractors till and sow the field; urea and DAP — both manufactured using natural gas as a primary feedstock — are trucked in and applied over the season; pesticides and weedicides, themselves energy-intensive to synthesise, are sprayed multiple times.

Cane and maize are heavily irrigated crops, and in most of India that means diesel pump-sets or grid electricity running for months, not the rainfall Brazil’s cane belt largely relies on. Harvesting machinery and haulage trucks burn more diesel still.

Inside the distillery, fermentation and distillation require sustained thermal energy, typically from a coal or biomass-fired boiler, plus electricity for the plant. And before a single litre reaches an engine, tanker trucks and rail wagons move finished ethanol out to blending terminals spread across the country — a transport leg that barely features in the efficiency claims made in Delhi.

The published numbers vary sharply by feedstock, and the gap matters given where India’s programme is headed. Sugarcane ethanol in Brazil — the global benchmark — is credited with a relatively favourable energy return, commonly cited at 6.5-to-1 to as high as 10-to-1, largely because mills burn leftover bagasse fibre to power distillation itself.

But Brazilian cane is grown predominantly under rainfall; Indian cane, concentrated in Maharashtra and Uttar Pradesh, is grown under heavy irrigation. A net-energy study focused on Indian conditions notes that sugarcane here is both water- and energy-intensive precisely because of that irrigated model, meaning the Brazilian ratio is not a like-for-like stand-in.

Corn-based ethanol in the United States required 29 per cent more fossil energy than it delivered as fuel, according to the widely cited Pimentel and Patzek analysis — a finding still disputed by industry-linked studies claiming a modest surplus.

Maize is the more urgent worry, precisely because it is the feedstock India’s programme has leaned into hardest in its most recent, fastest-growing phase. International net-energy research on maize ethanol is genuinely contested, and this article does not pretend the science has settled cleanly either way.

USDA-linked analyses report a modest positive energy ratio, on the order of 1.24-to-1 to 1.34-to-1. Other well-known assessments, most prominently Pimentel and Patzek, found the opposite — a net energy loss once the full cultivation-to-processing chain is priced in.

Even the more optimistic published figure leaves almost no margin once the additional, rarely counted energy of road transport to distilleries and onward distribution of finished ethanol is added on top. A separate, India-specific study — Hiloidhari and colleagues, 2021 — found that straightforward electricity generation returns more usable energy per unit invested than sugarcane ethanol, with a smaller water and carbon footprint besides.

There is a final piece of arithmetic worth sitting with. Even at E20, ethanol displaces only one-fifth of the petrol in every tank; the remaining four-fifths still requires the entire conventional chain of crude extraction, shipping, refining and distribution, unchanged.

The elaborate cradle-to-grave energy cost of growing, harvesting, fermenting, distilling and hauling ethanol is being spent to alter roughly a fifth of the fuel mix. If the marginal energy returns on the feedstock financing that fifth is thin, as it appears to be for maize, the energy case starts to look less like a transition and more like an expensive rounding error dressed up as one.

Chemistry 101: Why Fuel Gets Thirsty

Fig. 12 — Hydrophobic petrol vs. hygroscopic ethanol. Original schematic illustration.

Underlying the caution most of the ethanol-using world has exercised is a basic property of the two fuels being blended. Petrol and ethanol behave completely differently around water, and this is not in dispute in the technical literature the way some water-footprint figures are.

Petrol is hydrophobic — it does not mix with water. If moisture enters a petrol tank, it separates out and sinks to the bottom as a distinct, drainable layer, leaving the fuel above it largely unaffected.

Ethanol is the opposite: it is hydrophilic, or more precisely hygroscopic. It actively draws moisture out of humid air and out of any residual water sitting in storage tanks, pipelines and vehicle fuel systems, and mixes completely with that water rather than separating from it.

Petrol repels the water that enters a tank; ethanol dissolves it. That single difference in chemistry is the quiet reason most ethanol-blending countries have stopped at 10 per cent.

Once the water absorbed by the ethanol component exceeds what the blend can hold in solution — more likely in humid storage, in a tank left standing, or wherever infrastructure is older — a heavier water-ethanol layer separates out and settles at the bottom of the tank. That is precisely where a standard fuel pump draws from, delivering a watery mixture straight into the engine and producing rough running, hesitation and stalling.

Sustained contact with a water-ethanol mixture also corrodes metal fuel-system components and degrades rubber seals, gaskets and hoses faster than pure petrol does. This is a real cost across the large majority of India’s existing fleet, designed and calibrated before ethanol blending existed as a specification.

Ethanol itself carries meaningfully less energy per litre than petrol — on the order of a quarter to a third less — which lowers fuel economy on its own, before any moisture-related losses are added. Independent technical assessments put E20’s mileage penalty, in vehicles without flex-fuel tuning, at roughly 5 to 15 per cent.

A fuel that quietly lowers mileage forces a vehicle to burn more litres to cover the same distance, eating directly into the tailpipe-emissions savings the programme is built to claim. A fuel that corrodes components faster forces earlier replacement of pumps, injectors and lines, each carrying its own manufacturing footprint.

Government-backed testing, discussed further below, has found no major compatibility issues beyond earlier wear on certain rubber components in older vehicles — a narrower finding than it is sometimes presented as, but one describing exactly the failure mode this chemistry predicts. Brazil’s flex-fuel vehicles, built from the outset with ethanol-resistant lines and stainless tank internals, handle it without difficulty; India’s legacy fleet was not built that way.

Some Like It Hot — Engines Don’t

Fig. 13 — Design temperature vs. Indian summer ambient temperature. Illustrative comparison based on IMD summer data and standard seasonal RVP specifications.

There is a further chemistry issue that gets even less public attention than phase separation, and it matters more in India than in almost any other major ethanol-blending market: heat. Blending ethanol into petrol does not simply average the volatility of the two components; it raises the blend’s Reid Vapour Pressure above what a simple weighted mix would predict.

This is a well-documented effect in fuel-chemistry literature, and one an independent Indian analysis has specifically flagged in the context of E20. Global fuel specifications have historically managed this with seasonal RVP limits, tightening volatility rules each summer to prevent vapour lock and excess evaporative emissions.

Vapour lock occurs when fuel boils inside the lines or pump before reaching the engine, starving it of a consistent supply and causing stalling or hard restarting. Most of India runs considerably hotter, for considerably longer each year, than the temperate markets these volatility standards were originally built around.

Summer ambient temperatures of 40 to 45 degrees Celsius are routine across the Indo-Gangetic plain and much of central and western India, and fuel sitting in a tank or engine bay in that heat can reach temperatures well beyond ambient. That combination raises vapour-lock risk, particularly in India’s very large fleet of older, carburetted two-wheelers and small cars.

A more volatile fuel blend, in a country where summer heat is both more intense and more prolonged than in the United States or Europe, is precisely the combination that raises vapour-lock risk.

The same volatility increase raises evaporative VOC losses at exactly the time of year India’s cities can least afford them. Volatile organic compounds are ozone precursors, and ground-level ozone is already a serious warm-weather health hazard in Indian cities — layering a summer pollution pathway on top of the more familiar winter particulate crisis.

An independent analysis of India’s E20 rollout has also flagged that ethanol combustion tends to increase nitrogen oxide emissions and produce a measurable spike in acetaldehyde, a toxic carbonyl compound currently unregulated in India’s vehicle emission standards. Brazil, by contrast, has built specific monitoring protocols for exactly these compounds after decades of high-blend experience.

India has not yet done the equivalent. This is less a single defect than a climate-geography mismatch: RVP limits and emissions frameworks built and tested for temperate conditions have been extended to a tropical country running considerably hotter, without the localised testing that difference would seem to warrant.

When Savings Leak Out: A Gross Figure, Not a Net One

Fig. 14 — Illustrative index of offsetting import flows; no official netted figure is published.

This brings the argument back to the number the ministry leads with every time: crude oil import savings. That figure assumes, implicitly, that a litre of E20 does the same work as a litre of pure petrol — that every litre of ethanol blended in displaces a litre of imported crude-derived petrol one for one.

The mileage penalty described earlier undercuts that assumption directly. If a vehicle running on E20 needs roughly 5 to 15 per cent more fuel to cover the same distance, part of the crude oil ostensibly saved is being clawed back by the extra volume of blended fuel the vehicle now burns — an effect that does not appear in the ministry’s headline savings figure at all.

Even setting the mileage penalty aside, the forex case rests on treating avoided crude imports as a clean, uncontested gain, without netting out the new import lines the programme itself is now generating elsewhere. Maize imports, discussed earlier, surged to feed distilleries in a country that had historically been a net maize exporter.

Fertiliser is a second, less-discussed leak. India still imports the entirety of its muriate of potash and a large share of its DAP — Saudi DAP imports alone rose 17 per cent to 1.9 million tonnes in 2024-25 — feeding a Department of Fertilisers budget that topped roughly Rs 1.92 lakh crore in 2024-25.

Part of the foreign exchange the programme claims to save on crude is arguably being spent instead on the ships bringing in potash, DAP and urea from Canada, Saudi Arabia, Morocco, Russia and the Gulf.

A third, harder-to-quantify leak sits in the vehicle fleet itself. The accelerated corrosion and seal degradation described in the chemistry section means more frequent replacement of fuel pumps, injectors, hoses and gaskets, a share of which carries import content in India’s still not fully self-sufficient auto-components supply chain.

None of this is offered as a claim that the programme’s net import bill is worse than doing nothing — that would require a level of netted, published accounting that does not currently exist. The point is narrower: the ministry’s headline forex-savings figure is a gross number on one side of a ledger, not a net one.

A genuinely honest accounting would set the avoided crude import bill against the mileage penalty, the maize import surge, the fertiliser import content, and the additional vehicle-component wear the programme’s own chemistry produces. Only the netted figure, not the gross one, would say anything meaningful about whether E20 is reducing India’s total import dependence or simply moving which ships are doing the importing.

What the Ministry Gets Right — and Wrong

Fig. 15 — Based on the Ministry of Petroleum & Natural Gas’s July 2026 ten-point rebuttal.

It is worth taking the ministry’s rebuttal seriously rather than dismissing it wholesale, because parts of it are accurate. Ethanol plants genuinely do require statutory environmental clearances and are subject to Zero Liquid Discharge norms governing what a distillery can release back into a river or drain.

Automotive testing by the Automotive Research Association of India, run jointly with Indian Oil and SIAM, has found no major engine-compatibility issues in vehicles calibrated for E20, beyond earlier wear on certain rubber components in older vehicles. That is a narrower and more defensible claim than the sweeping “no issues at all” framing used in press conferences.

It is also true, as the ministry says, that Canada, Japan, Thailand and much of Europe already blend ethanol as a matter of routine, so India’s E20 is not some untested outlier. Where the defence becomes thinner is by conflating several distinct questions into one reassurance.

Plant-level compliance says nothing about whether the sugarcane or rice feeding a distillery was grown using water the region could not spare, or how much diesel and fertiliser-embedded energy went into growing it. The ministry’s point that paddy and cane are grown “primarily for food security” is genuine, but it sidesteps the fact that a growing share of cultivation, particularly maize, is expanding specifically because ethanol demand created the price incentive to grow more of it.

A Narrower, Smarter Path to Energy Security

Fig. 16 — Correctives already proposed by the institutions running the programme.

None of this argues for abandoning ethanol blending. The policy instinct is often sound; the execution is where the environmental bill quietly accumulates. Several correctives are already being proposed by the same institutions running the programme, and deserve to be the actual policy agenda rather than footnotes to a press conference:

- Basin-level water budgeting before, not after, distillery licensing — no new capacity in districts the Central Ground Water Board already classifies as over-exploited.

- Mandatory water-footprint audits published per distillery, not aggregated at state or national level.

- A hard ceiling on maize diverted from the feed pool, with duty-free imports permitted specifically for ethanol use and ring-fenced against leaking into food markets.

- Accelerated, funded investment in genuine second-generation capacity — not just approvals on paper — including solutions for the pretreatment wastewater and solid-waste streams 2G itself generates.

- An honest, third-party lifecycle emissions audit, cultivation to combustion, published alongside the tailpipe savings figure.

- A published, feedstock-wise net energy (EROEI) audit made a precondition for any blending increase beyond E20, rather than an afterthought once E85 and E100 are rolled out.

- A genuinely netted import-bill accounting — crude savings weighed against the mileage penalty, maize imports, fertiliser import content and vehicle-component replacement.

- India-specific summer vapour-pressure and evaporative-emissions testing across two-wheelers, three-wheelers and pump-set engines, before any move to E27 or higher blends.

The Uncomfortable Bottom Line: Out of the Pipe, Into the Aquifer

Energy security and climate accounting are not the same test, and a programme can pass one while quietly failing the other. India’s ethanol blending programme has demonstrably reduced crude import dependence and put real money into farmers’ hands — achievements that deserve acknowledgment, not dismissal.

Fig. 17 — Summary diagram synthesising the article’s findings.

But a fuel promoted as environmentally friendly, and as a foreign-exchange saviour, cannot be assessed only at the point of combustion or only on the crude side of the import ledger. The water drawn from stressed aquifers, the pulses and oilseeds displaced by maize, the rising cost of eggs and milk, the still-uncertain net lifecycle emissions — all belong on the same page as the tailpipe-savings figure.

So does a feedstock-wise energy return that looks thin-to-negative for the very crop the programme now depends on most; a hydrophilic-versus-hydrophobic chemistry mismatch made more acute by Indian summer heat than by the temperate climates the blending science was developed in; and an import bill that appears to be re-emerging through maize and fertiliser even as it recedes through crude.

The programme looks less like a clean climate solution and more like a transfer of environmental and economic cost — from the tailpipe, which is visible and easy to regulate, to the water table, the food basket, the energy books, the engine bay and a different page of the import statistics.

That is not an argument on ethanol controversy. It is an argument against treating a feedstock question as a fuel question, and against letting a genuinely useful energy policy borrow its legitimacy from an environmental claim it has not yet earned.

Bhuwan Mohan Prasad is an environmental consultant holding a Bachelor’s in Civil Engineering and a Master’s in Environmental Engineering from IIT Kanpur, along with two Master’s degrees from the University of Toronto — in Chemical/Environmental Engineering, and in Forestry/Composite Materials. His professional experience includes serving as Senior Environmental Engineer at the Central Pollution Control Board, New Delhi, and as Environmental Advisor with Ontario Power Generation, Toronto.

References

Ministry of Petroleum and Natural Gas, Government of India — Ten-point rebuttal on E20 ethanol blending, July 2026.

Ministry of Petroleum and Natural Gas — “Second Generation (2G) Ethanol,” Refinery Division policy page.

NITI Aayog — Ethanol roadmap and Composite Water Management Index reports.

Economic Survey of India, 2025-26 — Chapter on agriculture and cropping-pattern shifts.

USDA Foreign Agricultural Service, GAIN Report — “Biofuels Annual: India,” 2025.

Down To Earth — “DTE Exclusive Analysis: Rethinking E20,” March 2026.

Hiloidhari, M. et al. (2021) — Water, energy and carbon footprint of sugarcane bioethanol, India.

Energy assessment of second-generation (2G) ethanol production from wheat straw in the Indian scenario — PMC/NCBI peer-reviewed study.

Pimentel, D. and Patzek, T.W. — Net energy analysis of corn ethanol, widely cited US net-energy literature.

Praj Industries — “Enfinity” 2G ethanol technology documentation.

Central Ground Water Board, Government of India — groundwater stress classifications by district.

Reuters and other international newswire reporting — independent estimates of India’s ethanol-linked CO2 savings.

TradeInt / Government trade data — India fertiliser import statistics by source country, Q1 2026.

Press Information Bureau, Government of India — Department of Fertilizers budget and DAP import agreements with Saudi Arabia, 2025.

US Environmental Protection Agency — E15 summer-sales waiver notification, 2026.

European Union member-state fuel-quality reporting — E5/E10 blending status across member states.

Reporting on Brazil’s ethanol mandate history and 2025 blend-ratio increase to E30.

Automotive Research Association of India (ARAI), Indian Oil Corporation and SIAM — joint E20 vehicle-compatibility testing.

Fuel-chemistry literature on ethanol-petrol blend volatility and Reid Vapour Pressure non-linearity.

FAO — Market for Tropical Fruits in India (forex value of fruit exports vs. cereal crops).

Government of India / industry trade data — India edible oil import bill, 2023-26; pulses import statistics, 2024-25.

India guava export data, 2013–2023 — APEDA and trade-data aggregators (Seair Exim Solutions).

{kind=link}